How the Paycheck Protection Program in the CARES Act Works

The United States Treasury announced details for the Paycheck Protection Program authorized under the CARES Act signed into law on March 27, 2020.

For small businesses in the United States, these provisions are the most critical components of the CARES Act because it provides $349 billion in federally-guaranteed loans under the Small Business Administration’s (“SBA”) 7a program. The loan is intended to help small businesses retain employees and pay for other allowed expenses.

Businesses are able to use the loan to cover payroll costs including benefits, most mortgage interest, rent, and utility costs over the 8 week period after the loan is made. So long as loans are used for these purposes, loans will be forgiven if employee numbers and compensation are maintained during that time period or are returned to normal by June 30, 2020.

Loans can be for the lesser of $10 million or 2.5 times a business’s average payroll cost for a twelve-month period. Interest rates are fixed at 0.50%, payments are deferred for 6 months, and the loans are due 2 years from the loan date. No collateral is required nor is a personal guarantee required.

SBA-approved lenders will start processing borrower applications according to the following schedule: April 3, 2020, for small businesses and sole proprietorships; April 10, 2020, for independent contractors and self-employed individuals.

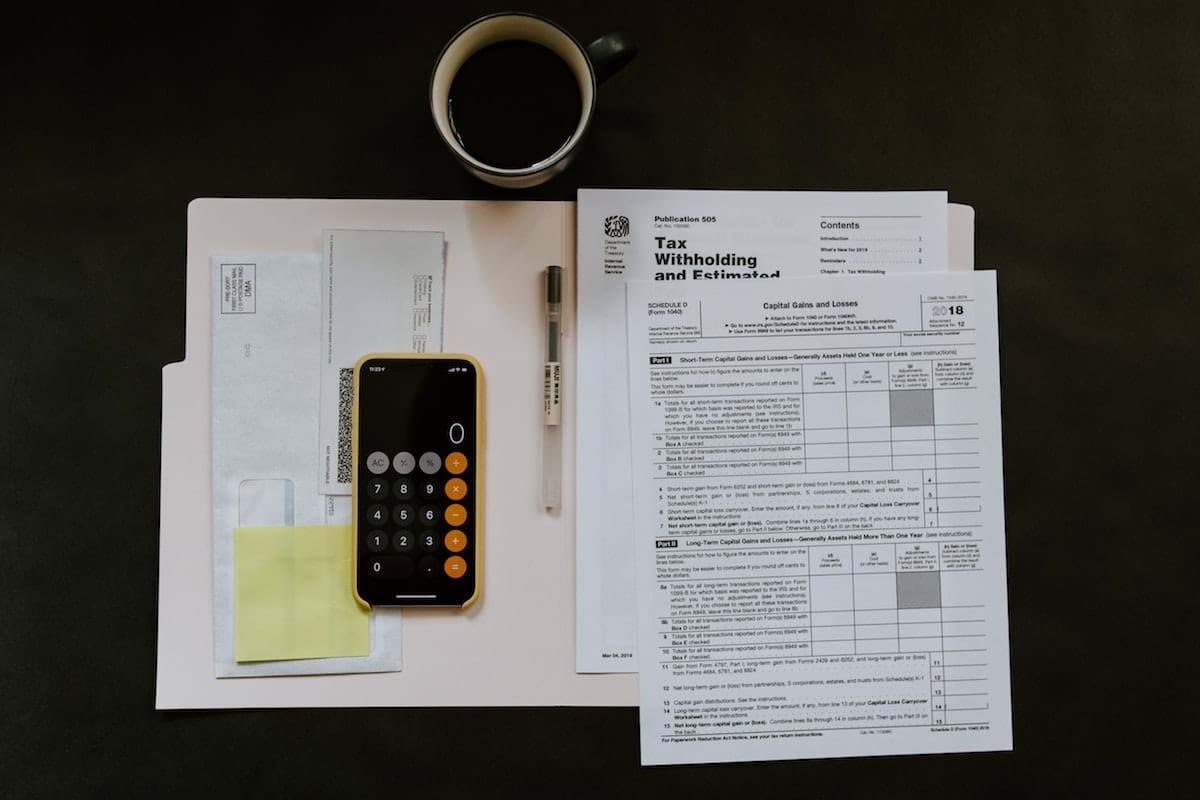

In the attached PDF, you’ll find additional guidance on the Paycheck Protection Program and examples of how to calculate loan amounts.

![]()

No Entries have been added yet.

We are working hard to get this ready for you. Check back soon for new entries!

Service Areas

- Who We Are

- ---Matthew McLaughlin

- ---Conner Reeves

- Industry Experience

- ---Cannabis & Medical Marijuana

- ---Craft Brewery & Distillery

- ---Food & Beverage

- ---Restaurants & Hospitality

- ---Manufacturing

- ---Technology

- ---Nonprofits & Social Innovators

- ---Startups & Emerging Companies

- ---Healthcare

- Service Areas

- ---Business

- ---Economic Development

- ---Employment

- ---Intellectual Property

- ---Real Estate & Development

- ---Trademark & Branding

- ---Venture Capital & Angel Investment

- Blogs

- ---Small Batch Blog

- ---Cannabis Law Blog

- ---News Blog

- Contact Us

- ---Jackson

- ---Birmingham

- Resources

- ---Legal Guides

- ---Videos

Industry Experience

- Who We Are

- ---Matthew McLaughlin

- ---Conner Reeves

- Industry Experience

- ---Cannabis & Medical Marijuana

- ---Craft Brewery & Distillery

- ---Food & Beverage

- ---Restaurants & Hospitality

- ---Manufacturing

- ---Technology

- ---Nonprofits & Social Innovators

- ---Startups & Emerging Companies

- ---Healthcare

- Service Areas

- ---Business

- ---Economic Development

- ---Employment

- ---Intellectual Property

- ---Real Estate & Development

- ---Trademark & Branding

- ---Venture Capital & Angel Investment

- Blogs

- ---Small Batch Blog

- ---Cannabis Law Blog

- ---News Blog

- Contact Us

- ---Jackson

- ---Birmingham

- Resources

- ---Legal Guides

- ---Videos

Who We Are

- Who We Are

- ---Matthew McLaughlin

- ---Conner Reeves

- Industry Experience

- ---Cannabis & Medical Marijuana

- ---Craft Brewery & Distillery

- ---Food & Beverage

- ---Restaurants & Hospitality

- ---Manufacturing

- ---Technology

- ---Nonprofits & Social Innovators

- ---Startups & Emerging Companies

- ---Healthcare

- Service Areas

- ---Business

- ---Economic Development

- ---Employment

- ---Intellectual Property

- ---Real Estate & Development

- ---Trademark & Branding

- ---Venture Capital & Angel Investment

- Blogs

- ---Small Batch Blog

- ---Cannabis Law Blog

- ---News Blog

- Contact Us

- ---Jackson

- ---Birmingham

- Resources

- ---Legal Guides

- ---Videos

Blogs

- Who We Are

- ---Matthew McLaughlin

- ---Conner Reeves

- Industry Experience

- ---Cannabis & Medical Marijuana

- ---Craft Brewery & Distillery

- ---Food & Beverage

- ---Restaurants & Hospitality

- ---Manufacturing

- ---Technology

- ---Nonprofits & Social Innovators

- ---Startups & Emerging Companies

- ---Healthcare

- Service Areas

- ---Business

- ---Economic Development

- ---Employment

- ---Intellectual Property

- ---Real Estate & Development

- ---Trademark & Branding

- ---Venture Capital & Angel Investment

- Blogs

- ---Small Batch Blog

- ---Cannabis Law Blog

- ---News Blog

- Contact Us

- ---Jackson

- ---Birmingham

- Resources

- ---Legal Guides

- ---Videos

Do you have a minute?

We would love to have your honest review of the experiences you have had with our company. Please review us on google business.